Predators are most dangerous when wounded

Exploring the second order effects of last weeks AI-driven tech stock crash

Enterprise technology companies have always been among the most aware and dangerous organisations in any market. They are conditioned for fierce competition. Their venture capital-backed models reward winner-takes-all thinking, and they will chart a course to survive at all costs.

I have spent nearly 20 years in financial services technology, and in that time I have watched these companies operate up close. They use every advantage available to create product lock-in, protected by their lines of code and their moats of user data, making switching nearly impossible. If you have ever sat across the table from an enterprise software vendor during a contract renewal, you know the most humbling feeling in business: the realisation that they hold the leverage.

The bigger the customer, the more data, the harder to move, the bigger the software vendor’s leverage. Their prey are often less technically capable customers who are on the back foot from the outset, locked into multi-year contract frameworks designed to suit the vendor, not the buyer. Often, these customers are forced to accept price rise after price rise with no realistic transition plan out.

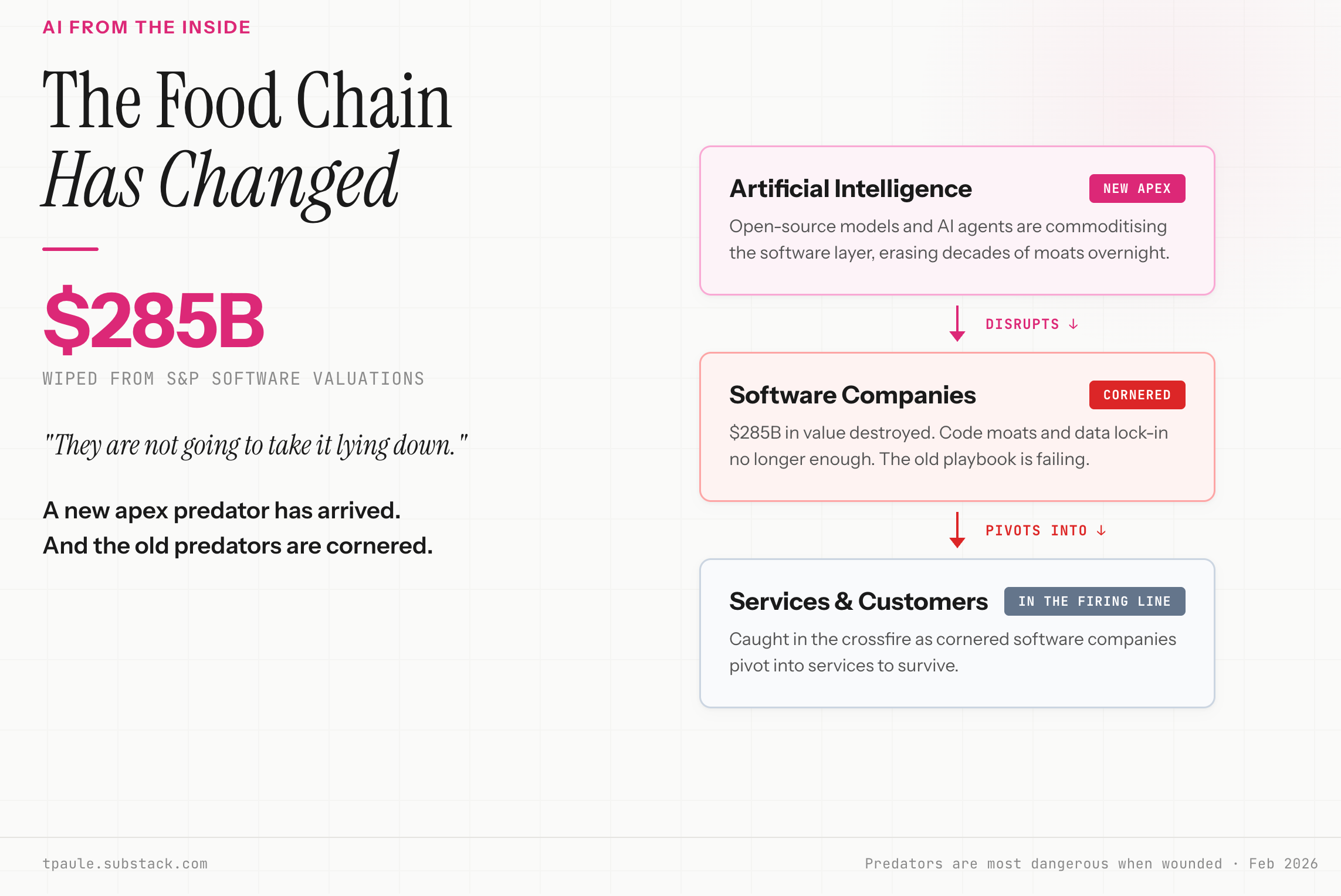

Something changed last week. These same software companies, the ones accustomed to being at the top of the food chain, were humbled themselves. Collectively, they had $285 billion wiped off their value in the S&P alone. The entire market has realised there is a new apex predator, and it is called Artificial Intelligence.

This article explores what happens when some of the most capable and dangerous organisations in the market are cornered and wounded. It unpacks what the software companies’ response is likely to look like, and who is in the firing line. Because one thing is certain: they are not going to take it lying down.

Let’s jump in.

What happened: ‘The Wreckage’

Earlier this week, a 200-line markdown file just wiped $285 billion in market value.

This file, called “knowledge-work-plugins/legal”, contains roughly 200 lines of structured prompts, first-year law school content with some clever workflow logic. It was shipped as an open-source plugin for Anthropic’s Claude Co-work. It can triage NDAs, flag non-standard clauses against a negotiation playbook, and generate compliance summaries. The kind of work that, until that week, required a paralegal, a series of expensive software subscriptions, and billable hours.

By Monday morning, Thomson Reuters had posted its biggest single-day stock decline on record. RELX, the parent of LexisNexis, fell 14%. LegalZoom cratered 20%. The selling spread to private equity from there: Ares Management, KKR, and TPG all dropped roughly 10%. If AI compresses the cost of legal and financial analysis, then every firm charging premium fees for that analysis has a margin problem that starts right now, not some unknown time frame in the future.

Let’s look at the data

Company: Thomson Reuters

Sector: Legal Tech

Recent Valuation Impact: -20%

Details: Biggest single-day decline on record; AI legal tools threaten paralegal workflows

Company: Figma

Sector: Creative Software

Recent Valuation Impact: -13% recent; -80% from all time high

Details: AI reducing the need for human design seats

Company: Atlassian

Sector: Collaboration Software

Recent Valuation Impact: -9.3% session; -59% peak-to-trough

Details: Trading at lows, down 34% YTD on agent fears

Company: HubSpot

Sector: Marketing Software

Recent Valuation Impact: -11.5% recent; -94% peak-to-trough multiple compression

Details: Seat-model vulnerability fully exposed

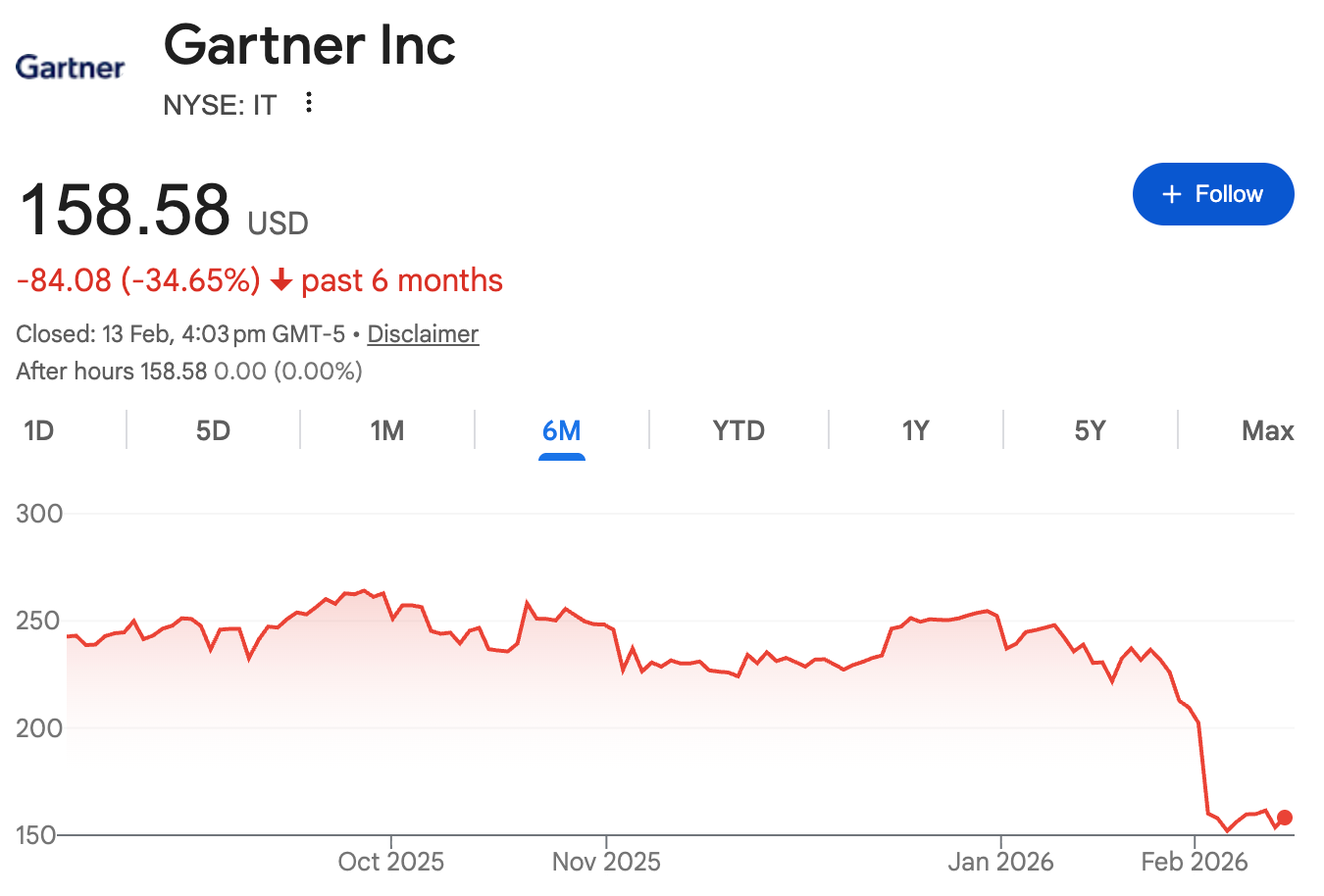

Company: Gartner

Sector: IT Advisory & Research

Recent Valuation Impact: -71% over 52 weeks; -21% single session (Feb 3)

Details: Beat Q4 earnings but stock cratered on weak 2026 guidance; clients replacing advisory services with AI tools

The picture is clear

In total, approximately $285 billion in value was wiped from S&P software and data stocks in 48 hours. Forward revenue multiples for SaaS companies dropped to historic lows of 3.9x. Free cash flow multiples compressed to levels we have never seen, despite many of these companies being solidly profitable.

It has already been dubbed the “Claude Crash.”

But the crash itself is not the story I want to tell. That is the first order effect, and while it is dramatic, it is also the part that most people are already talking about. The second order effect is far more consequential, and it is coming for every services business, every knowledge worker, and every professional who trades expertise for money.

Let me explain.

A predator is most dangerous when wounded

Here is what $2.2 trillion worth of software companies look like when their core revenue model starts breaking down.

Their economics are deteriorating in real time. When your revenue depends on selling seats to humans, and AI agents can now do that at a fraction of the cost, every licence renewal becomes a negotiation your customer does not want to have.

Investors can no longer model terminal value with any confidence because nobody knows what the competitive landscape looks like months, let alone years, from now.

Open-source agents are driving deflationary pressure that could compress SaaS spend from 10% of an employee’s salary to 1%. And the closed data architectures that companies like Salesforce built their moats around are becoming liabilities, because AI agents work best when they can move freely across systems, not when they are locked inside a single vendor’s silo.

The old playbook is not just outdated. It is actively working against them.

Naturally, there are counter views. Jensen Huang, speaking at the Cisco AI Summit just days before the crash, offered the strongest version of the counterargument: “This notion that the software industry is in decline and being replaced by AI is the most illogical thing in the world,” he said. His reasoning is simple: AI does not replace software, AI runs on software. The more agents you deploy, the more databases, APIs, and middleware you need. Every AI agent that replaces a paralegal still needs Thomson Reuters data, still needs a CRM, still needs document management.

Jensen is not wrong. He is also not making the argument he thinks he is making. Nobody serious is arguing that the world needs less software.

Instead, the argument is:

“The world no longer needs to pay for software the way it currently pays for software.”

Jensen is defending the product, the market is attacking the pricing model. Those are very different things, and confusing them is how incumbents lose transitions they should have survived.

Print media made this exact mistake. Newspapers had content people wanted: local information, investigative journalism, weather. The internet did not make that content worthless. What the internet did was destroy the access model, the idea that you had to buy a whole newspaper to get the one section you cared about. The content survived, the business model did not.

These companies are cornered. But cornered beasts do not lie down and die. They pivot. They attack. And they go after the one market large enough to sustain their growth ambitions: The global services economy.

What’s next? The move from Licences to Labour

This is the second order effect that most people are not yet seeing.

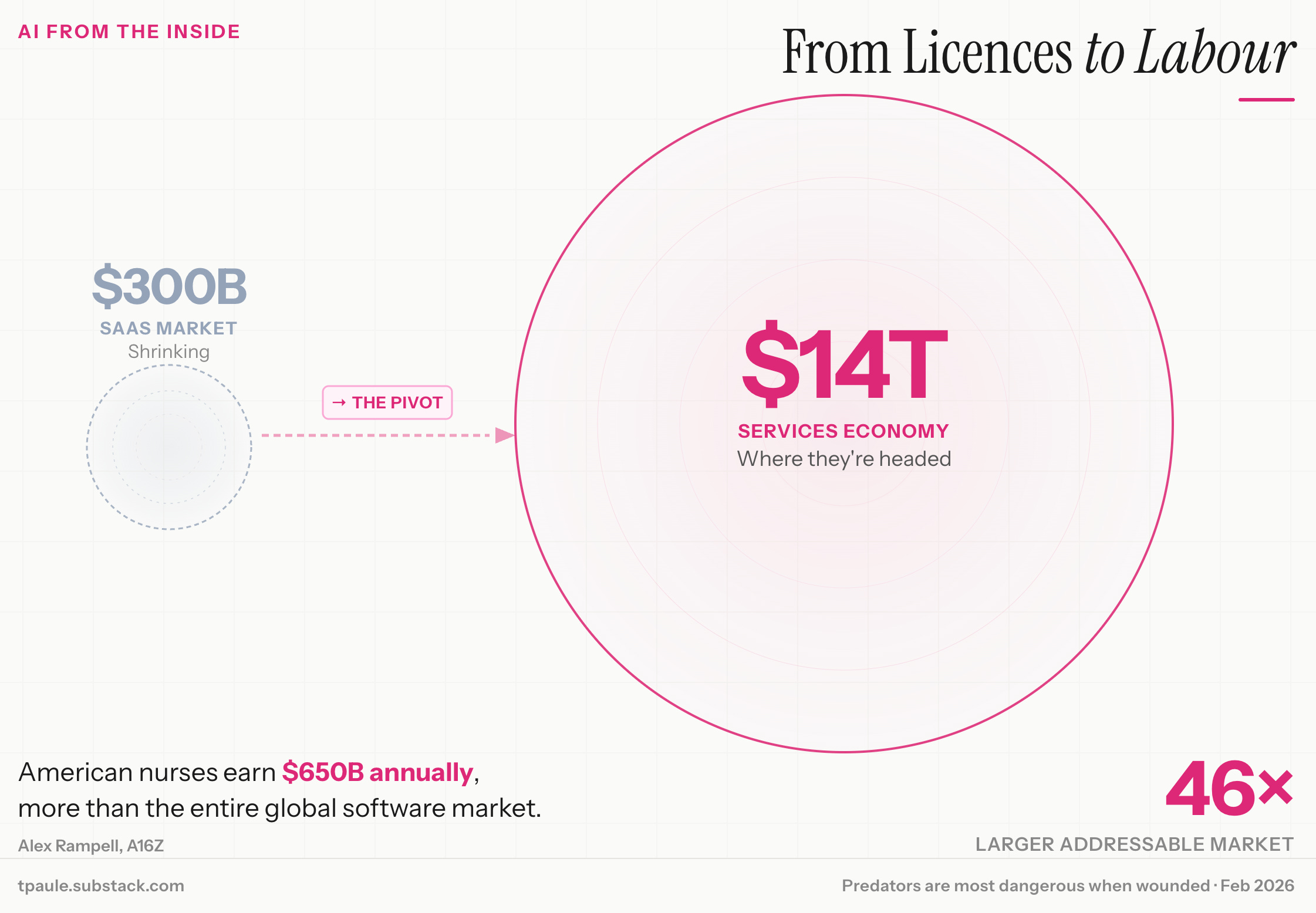

According to Andreessen Horowitz in their presentation ‘Software is Eating Labour’, the worldwide SaaS market generates roughly $300 billion in annual revenue. That is the ceiling these technology companies are bumping up against, and it is shrinking as AI compresses the value of traditional software. On the other hand, the U.S. labour market alone is $13 trillion. Alex Rampell from A16Z frames it well: American nurses earn $650 billion annually, more than the entire global software market. When software moves from selling tools to performing labour, the addressable market expands by orders of magnitude.

Software companies are not going to accept a slow decline in seat-based revenue. They are going to come for new revenue opportunities to replenish their losses, in the services layer. Every consulting engagement, every outsourced process, every knowledge worker role that involves research, analysis, drafting, coordination, or decision support is now in play.

I have been thinking about this shift for a long time. I actually wrote about it back in 2021, coining the term Service as a Software to describe what happens when software stops being a tool and starts delivering the outcome directly. I wrote this in a world that was pre-AI and therefore the prediction was probably five years too early. The infrastructure was not ready, models were not capable enough and the market didn’t yet believe it.

However, that has all changed now and the market believes it too. $285 billion evaporated in 48 hours.

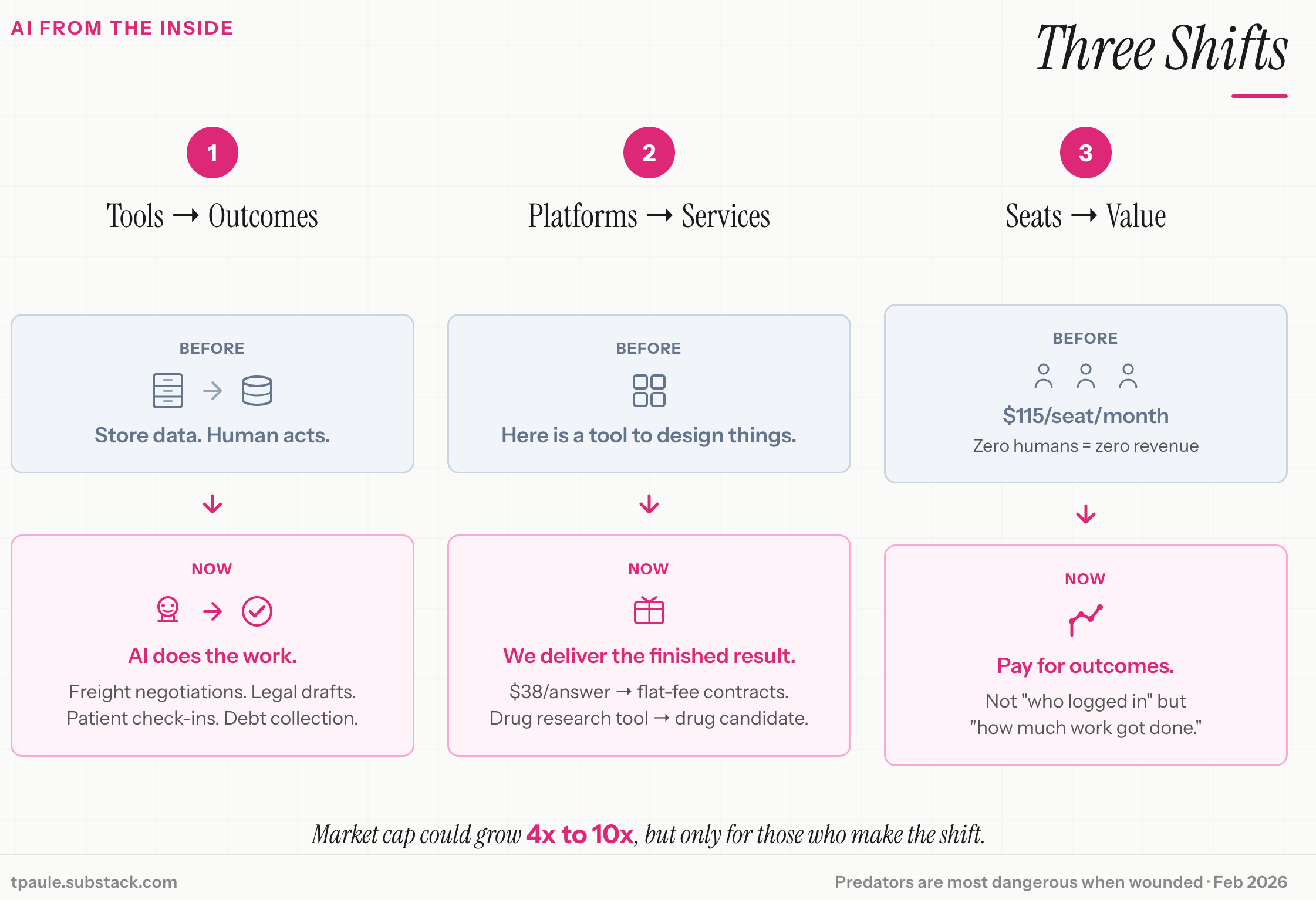

This transition can be understood through 3 shifts:

1. From Tools to Outcomes.

For the last several decades, the software industry built $2.2 trillion in market capitalisation by doing one thing: taking physical filing cabinets and turning them into databases. Salesforce stored your sales leads. Workday stored your HR records. Zendesk stored your support tickets. A human would then read the information and act on it. That era is ending. Software is no longer just enhancing worker productivity, to remain relevant and competitive it needs to move into completing the work. AI agents are now conducting live freight negotiations, performing post-surgery patient check-ins, drafting legal contracts, running automated reference checks, and handling multilingual debt collection calls in languages a human call centre could never staff for. This is not automation of existing tasks, this is the creation of entirely new capabilities.

2. From Platforms to Services.

As software begins delivering finished results rather than providing a platform for human labour, SaaS companies will effectively start absorbing the global services economy. They will look and act like service firms, where the value provided is the completion of a specific business objective. The shift from “we sell you a seat to design things” to “we design the airplane.” From “here is a tool for drug research” to “here is a drug candidate.” Customer support is moving from a $38 cost-per-answer model to flat-fee “all support handled” contracts. These are not hypotheticals, they are production deployments.

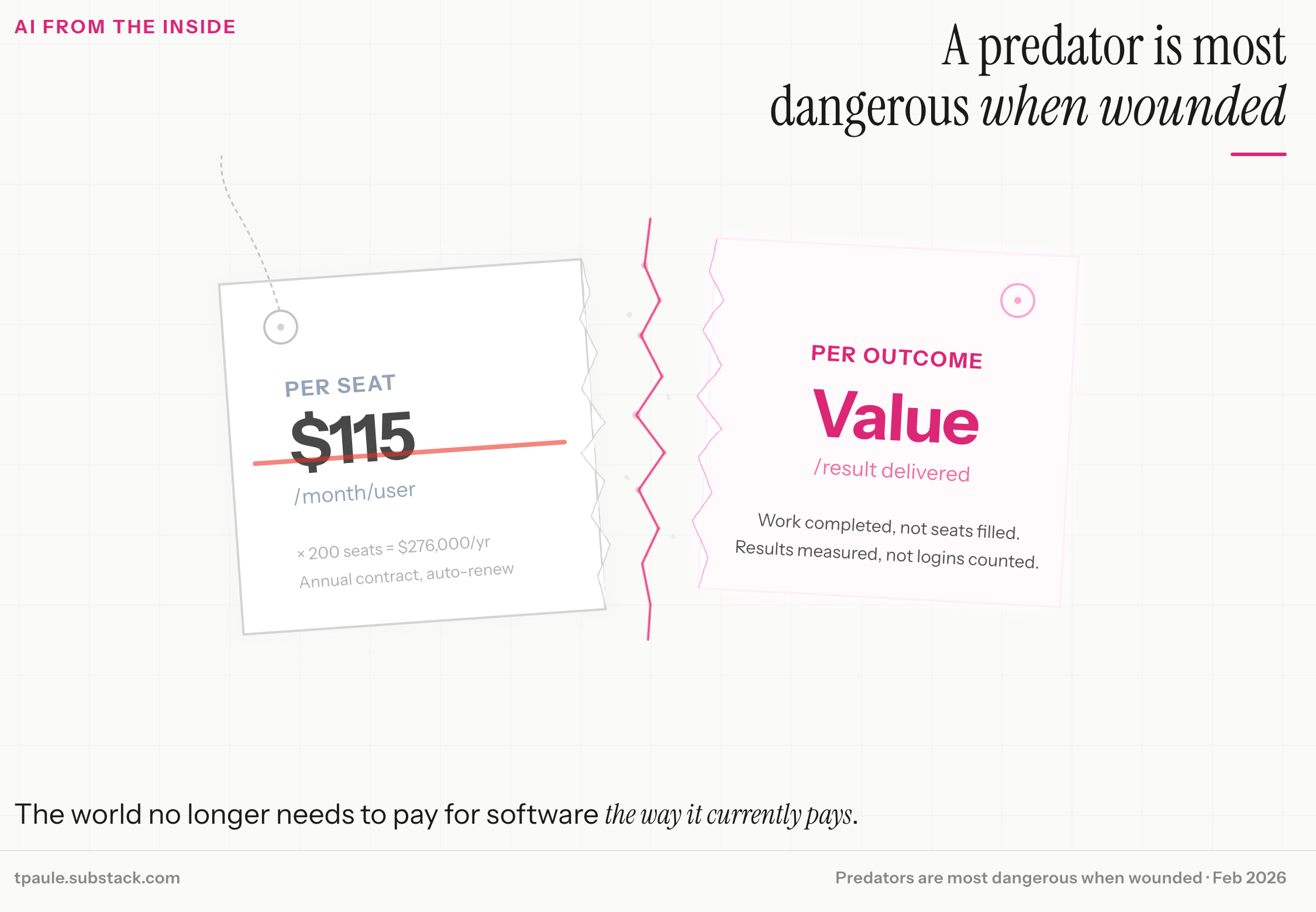

3. From Seats to Value.

The “per seat” licensing model is becoming a liability. If Zendesk charges $115 per month per seat, and AI makes agents productive enough that a company needs zero human seats, revenue drops to zero. The pricing model breaks. The replacement is value-based pricing, where costs are tied to the specific outcome delivered. Not “how many people logged in,” but “how much work got done” and “what was the result.” This rewards companies that deliver measurable, high-value outcomes rather than those that simply provide the prettiest interface. A16Z suggests total software market capitalisation could grow 4x to 10x over the next five years. But that growth will be concentrated in companies that successfully make this transition from tool provider to outcome provider. The rest will be left behind, squeezed between AI-native competitors above and open-source agents below.

This is what cornered, capable predators do. They do not shrink. They expand into new territory. And the territory they are coming for is the $14 trillion global services economy.

Every services business needs to understand this.

Software invading Services.

New Competition = Margin Compression

If you run a services business, everything I have just described should have your full attention. Software companies worth trillions of dollars, backed by the most sophisticated investors on the planet, are about to redirect their entire business models toward doing the work your firm currently does.

And the pressure is not just coming from software companies pivoting into your space. It is already showing up in your fee negotiations.

While everyone was watching Thomson Reuters’ stock price collapse, a quieter story broke that almost nobody paid attention to. KPMG, one of the Big Four accounting firms, pressured Grant Thornton UK, its own auditor, to cut audit fees. The demand was explicit: “pass on cost savings from AI”. Grant Thornton initially resisted, arguing that high-quality audits rely heavily on expert human judgment and that fees reflect the cost of people. KPMG’s response, per the Financial Times: “lower your prices or we’ll find a new auditor.” Grant Thornton blinked. KPMG’s international audit fees dropped from $416,000 in 2024 to $357,000 in 2025. A 14% discount.

That story matters more than any stock chart. The SaaS crash was a market event: traders repricing stocks based on a changed view of the future. The KPMG negotiation is an operating event: a real company using AI as a lever in a real business negotiation to extract a real price reduction from a real counterparty. The stock market repricing could reverse tomorrow, the KPMG precedent will not.

Think about what KPMG actually did. They did not automate their audit. They did not replace Grant Thornton with AI. They used the existence of AI, the fact that everyone now knows these tasks can be done more cheaply, as a negotiating weapon. The threat is not “we’ll replace you with AI.” The threat is “we both know AI changes the economics, so your old prices are not justified anymore.”

If audit fees get renegotiated on the basis of AI cost savings, legal fees can be next. Then consulting fees. Then implementation fees. Then design fees. Then every form of professional services billing that currently scales with the number of humans touching the work. The cascade does not require anyone to actually deploy AI at scale. It just requires buyers to point at the Claude Crash and say, “We know the world changed. Let’s talk about your rates.”

So the beasts are coming from two directions. Software companies are pivoting into your territory to find new revenue. And your existing clients are going to increasingly use AI as leverage to renegotiate your fees and compress your margins on the work you already do.

The Moat You Did Not Know You Had

But here is what most people miss: services businesses have one clear moat that software companies are still struggling to replicate:

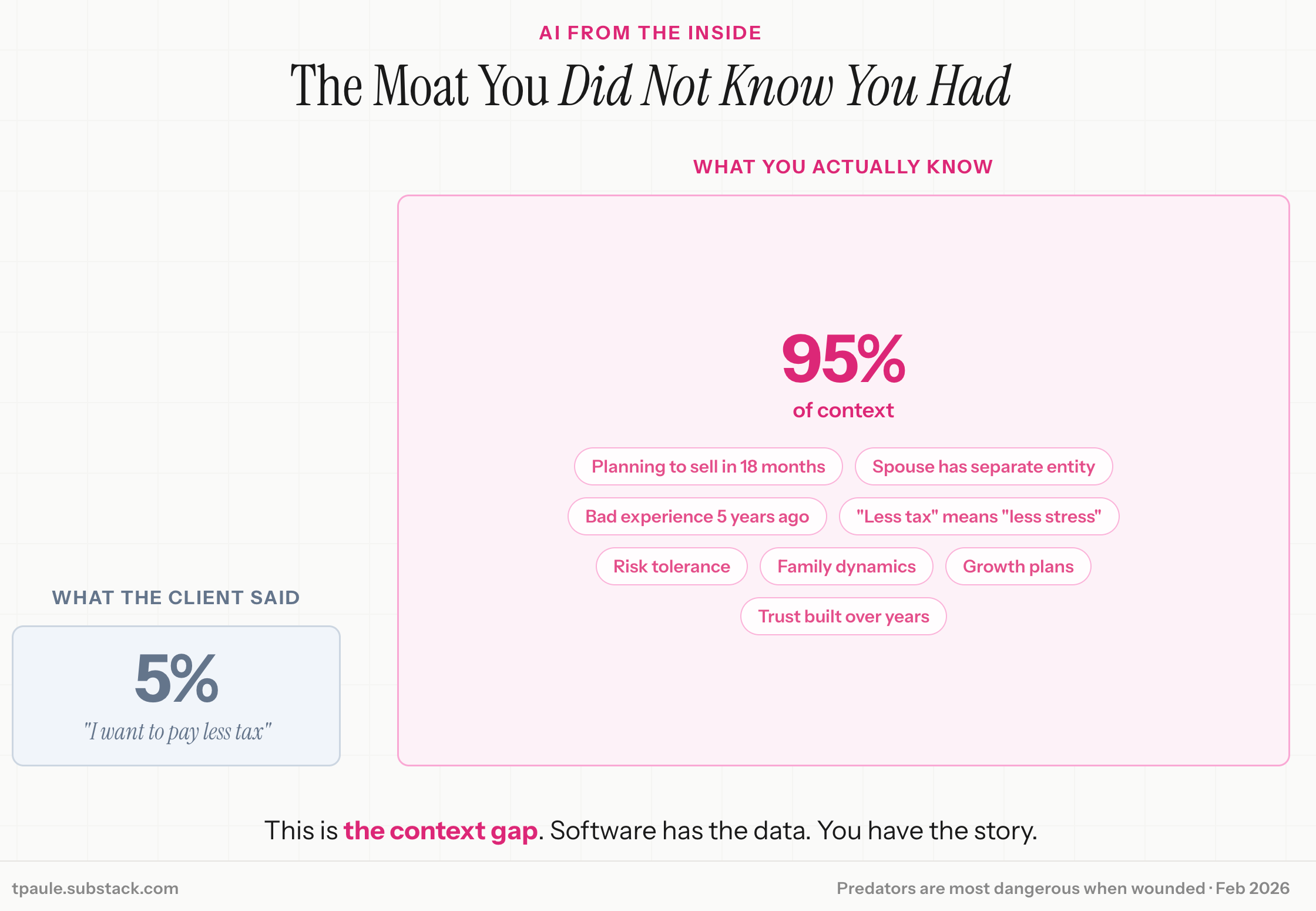

Customer relationships. And specifically, the context those relationships generate.

When a business owner tells their accountant “I want to pay less tax,” that sentence contains less than 5% of the information required to actually help them. The other 95% lives in context that no software system alone can captures: that they are planning to sell the business in eighteen months, that their spouse runs a separate entity with interrelated transactions, that they had a bad experience with an aggressive strategy five years ago and now prefer conservative positions, that “less tax” actually means “less stress at tax time.”

A good accountant builds this picture over years of conversations, quarterly reviews, offhand comments during coffee, and the slow accumulation of trust. It is a fundamentally different data set from the ledger, the trial balance, and the tax return. Enterprise software holds the financial data. The accountant holds the context that makes that data useful.

Whether an AI agent can acquire that same depth of context, not just process the numbers but understand the person behind them well enough to make the right judgment calls, is one of the biggest open questions in this entire transition.

And that is where services businesses have an advantage they may not even realise they hold.

Relationships are context firehoses. Every conversation, every meeting, every quick email exchange generates data that makes AI agents dramatically more effective. This is the moat that services businesses need to recognise and protect.

Services businesses that understand this will thrive. They will use AI to supercharge their existing client relationships, delivering outcomes at a speed and quality level that pure software plays cannot match. They will become the orchestration layer, the humans who ask the right questions and point the agents in the right direction.

Because in this new world, the value is not in having the right answers. It is in asking the right questions. The professional who knows which question to ask, what context to provide, and how to interpret the output will be exponentially more valuable than the one who simply knows how to use the tool.

The Clock Is Ticking

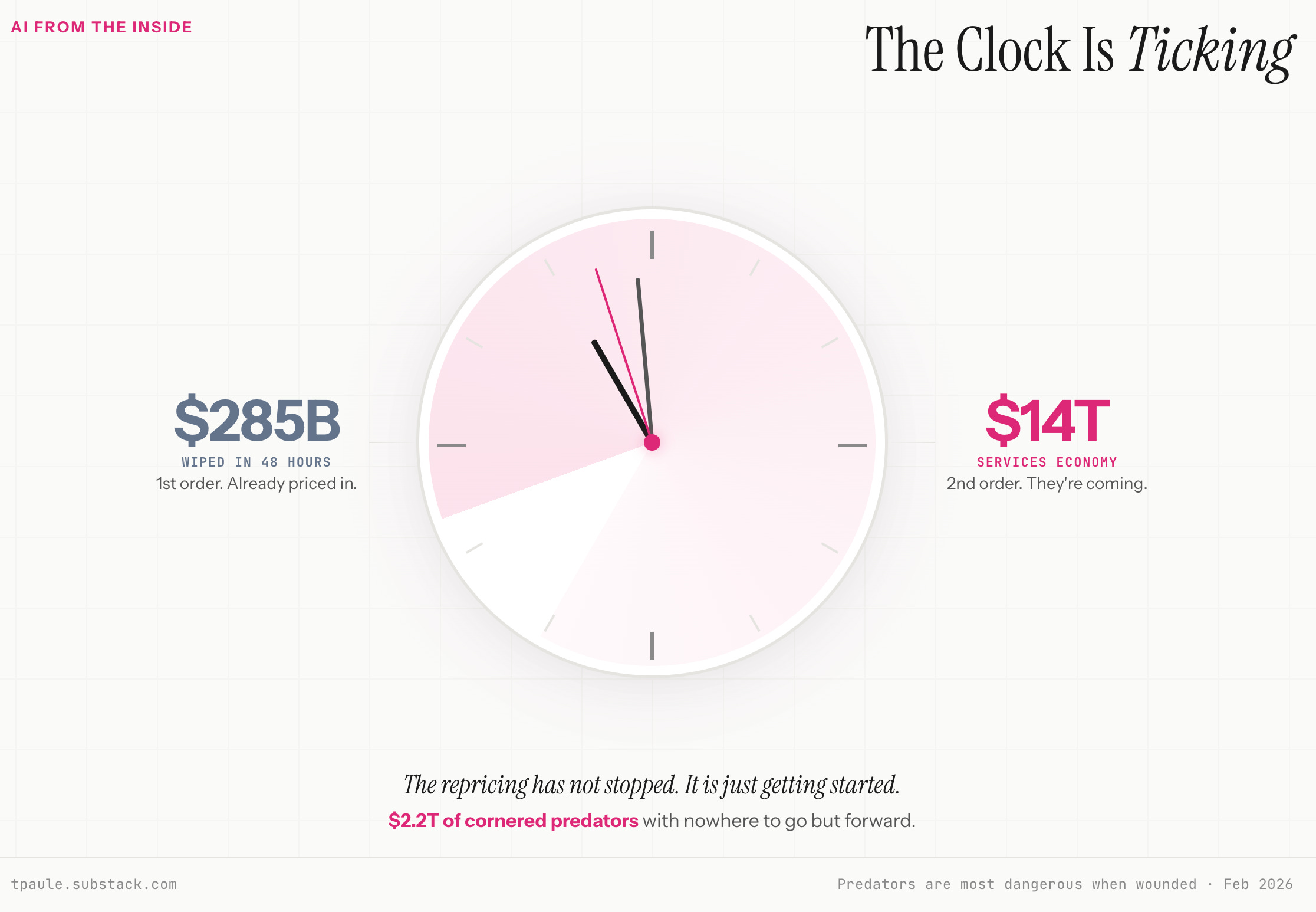

We are witnessing a once-in-a-generation repricing of the software industry. $285 billion vanished in 48 hours. Seat-based licensing, the revenue engine that powered three decades of SaaS growth, is changing before our very eyes.

That is the first order effect. It is dramatic, and it is already priced in.

The second order effect is the one that should keep services businesses up at night. Trillions of dollars in software market capitalisation is now searching for a new growth story. These companies have the engineering talent, the distribution, the capital, and increasingly the AI capability to deliver finished work, not just the tools to do it. They are cornered, and they are coming for the $14 trillion services economy. At the same time, your existing clients are already using AI as a negotiating weapon to compress your fees, whether or not they have actually deployed a single agent.

Client relationships, the trust, the context, the institutional knowledge built up over years of human interaction, are the one asset that AI cannot yet replicate from scratch. But it can amplify them beyond anything you have imagined. The question is whether you will be the one wielding that advantage or the one watching a software company take it from you?

A 200-line markdown file did not decide who wins and loses. But it did compress a transition that everyone expected to take five years into a 48-hour repricing event. And the repricing has not stopped. It is just getting started.

Service as a Software is a theoretical concept I dreamed up five years too early. Things have changed. It’s happening now, driven by the most powerful force in business: $2.2 trillion worth of cornered predators with nowhere to go but forward.

The clock is ticking.

Sobering and poignant analysis.

GT UK needed to be in a position where they were already 14+% more efficient in their service delivery before they got the call. A good example of the importance first/fast mover advantage as the chips fall in the coming months(weeks?).

Strap in!